INTRODUCTION

Hello again to our Q Report followers and fans of Victoria real estate — you have before you the real estate report REALTORS® read.

What Actually Happened. It’s not a question, it’s a statement — and we’ll get to that in detail shortly. Perhaps more importantly, let’s consider What is Actually Happening Right Now? That is definitely a question that is top of mind for many market watchers as we move into the latter months of 2023. What we see happening is plenty of — if not uncertainty, at least — hesitation. Latent demand remains high but at the same time buyers are becoming much more price sensitive. Mortgages being the largest household expense in Canada, this comes as no surprise, and even less so considering additional inflationary factors which have a lot of people who would otherwise be considering a move to ‘riding it out.’ Multiple categories of consumer debt are on the increase as well, and we may finally be seeing the early stages of a protracted slow down in the housing market as a result. Past history however shows us that this may not last for long.

THE EXPLAINER

Fall(ing) Market?

- As you will see in the market overview data, many of our Y/Y metrics show little change, which at first glance suggests a very stable market, however Q/Q changes speak to a softening trend in the nearer term.

- Our previous report on the spring market questioned whether the strength of 2023’s Q2 market represented a ‘dead cat bounce’ — a characteristic short-term rally where a given market, having begun to decline, appears to recover before ultimately continuing its downward trajectory.

- Of course, every point in each market cycle presents unique pockets of opportunity. We are happy to help you determine where yours lies if you are thinking of taking advantage.

- The current market is challenging to predict, to say the least. It is too soon to tell if early 2023 was a short-term rally, or a signal of stronger underlying resilience in the housing market. Macroeconomic conditions right at the top of Q4 bring us a few headlines that portend the potential for pain ahead:

- The bond market has been experiencing what some analysts have called a ‘meltdown’ at the time of this writing. The result: higher fixed mortgage rates. With the lowest posted rates now all well above 6%, the B-20 qualifying rates are all now well above 8% for borrowers. No surprise that activity is flagging.

- Canada has always relied on the housing sector for a large share of GDP. According to Statistics Canada, the portion of ‘residential investment’ making up GDP fell 13.8% Y/Y from 2022-2023. The last time Canadian investment in housing dropped this quickly, it foreshadowed the correction experienced in the late 1980s.

- Oxford Economics’ latest report indicates that Canada will be in recession until Q2 2024. They further predict that home prices nationally will continue to correct during this time as unemployment rises and financing rates remain high.

- In an interview with BNN/Bloomberg, former BoC Governor David Dodge said he believes rates will likely begin to come down in the latter half of 2024, ultimately settling somewhere around 3.5%, as he believes it is unlikely our economy can return to the 1-2% range long-term.

- BNN Bloomberg further reports that numerous sectors are already seeing a downturn in consumer spending, with S&P 500 companies expected to see declining profits by year end.

- Adding to supply woes, CMHC’s data indicate that housing starts were down significantly over the summer, registering -53% Y/Y in July for Greater Victoria.

- As we have mentioned before, interest rate movements tend to really manifest within markets 12-18 months later, so we still have yet to see the full effect of the most significant rounds of increases.

- Current mortgage trends provide further clues

- Despite eye-watering interest rates, statistics show mortgage arrears are at a decades-low level. The federal government has been pressuring banks to keep homeowners in their homes even when they have difficulty paying.

- However, if you asked the BoC, they would probably say that higher rates are supposed to be hard on borrowers

- At times we have seen the federal government working cross-purposes with the BoC. The BoC’s work to tamp down an inflationary cycle has been somewhat stymied by a government trying to protect citizens from effects of economic cycles.

- Case in point: there are Canadian mortgage holders whose amortizations have pushed beyond 100 years.

- At least the government’s own heavy debt service costs are necessarily slowing the flow of ‘helicopter’ stimulus money

- However, ongoing mortgage relief will continue to artificially prop up a housing market that technically should be much worse off, until significant unemployment comes into the picture

- For now, we continue extending and pretending, but when will the pretending be ending?

- Teasing some timely data from our own real estate market data, we decided to revisit two metrics we have assessed in past editions to gauge trends in supply and demand: MOI (months of inventory) and SNLR (sales to new listings ratio).

- MOI: Generally speaking, most analysts consider the range of 4-6 months of inventory to represent a ‘balanced’ market without significant pressure on prices either way. Though we still hold the memories of white-knuckling our way through a pandemic market where MOI dropped below 1, we have seen this figure rising rapidly, especially at the end of Q3, rapidly approaching 4.0 for the local market as a whole, and already well above 5.0 in some areas such as the Westshore, signalling a market shift out of the hands of sellers.

- SNLR: Imagine 100 homes are listed this month, and 40 of them sell this month. The sales to new listings ratio is 0.4, or 40%. As this ratio gets smaller, standing inventory increases, and MOI goes up. In our example, 60 of the homes listed and not sold are carried into next month as standing inventory. Below is the trend over the past two quarters for our local market as a whole; note that it looks like the inverse of the MOI curve above.

- Analysis of SNLR generally regards the ~60%+ range to be a sellers’ market, and the ~40%- range to be a buyers’ market. By these metrics, Q3’s counts of sales to new listings suggests the same trend as MOI, though this points more strongly toward edging into a buyers’ market.

- We will continue to monitor these trends and report whether what we’re recording is a slight exaggeration of market seasonality, or the proverbial canary in the coal mine.

- Stimulative levels of immigration and the low count of housing units per capita may ultimately continue to hold a ‘crash’ at bay, though an increasing number of Canadians are reporting increased housing-related financial stress.

- A recent Zolo survey indicated more than 90% of housing market participants agreed that some degree of FOMO influenced their decision-making.

- When asked if they worried about being able to afford their mortgage when it comes up for renewal, the responses spoke strongly, with nearly 80% saying they worry sometimes, often, or all the time:

MARKET BREAKDOWN

Overview

- Overlaying strata, detached homes and luxury listings, we see that there are similarities in nearly all the metrics we record across segments. Listing inventory managed to grow, and, despite this increase in available homes, pricing remained firm, ticking up slightly across all property types Y/Y.

- But, considered against the backdrop of inflation, where CPI was up 4% Y/Y in August, the apparent increases in sale prices are either barely keeping up with inflation (if you happen to be in the single family home market), or the inflation-adjusted value of your condo or luxury property is beginning to slide.

Detached Homes, <$1.5M

- The statistics for sales of single-family detached homes around the region show little movement year over year, but it was the Q/Q turn that caught our attention, as in this segment, we see signs of a softening market in every metric.

- Sales down, prices down, market times up, listing discounts up, and inventory increasing, all at once.

- Were it not for the roller coaster-like figures of our historical counts, we may be tempted to chalk this up to regular market seasonality.

- These figures are certainly not indicative of a plummeting market, though perhaps are empirical evidence of the slow market we’ve been hearing about anecdotally around the office water cooler this summer.

Strata Homes, <$1.5M

- We see a similar story playing out in condo and townhouse sales to the detached homes market, though the strata segment continues to perform relatively well given its more accessible price point in a higher rate environment, and the pace of sales has made a buildup of standing inventory relatively slower.

- It is typical to see a decrease in sales volume from Q2 to Q3, and we saw a doozy last year as a series of rapid fire rate hikes took effect.

- However, the number of sales dropping by more than 25% Q/Q — as we covered in The Explainer, above — caught our attention.

- Prices softened very slightly from Q2, and showed a slight uptick Y/Y, suggesting pricing in the strata market has been more stable even as mortgage rates have continued to go up.

Luxury Homes, >$1.5M

- Uniquely within the luxury segment were increases in median price and price per square foot compared both with last quarter and with last year.

- But like strata and detached sales, both market times as well as listing inventory are increasing.

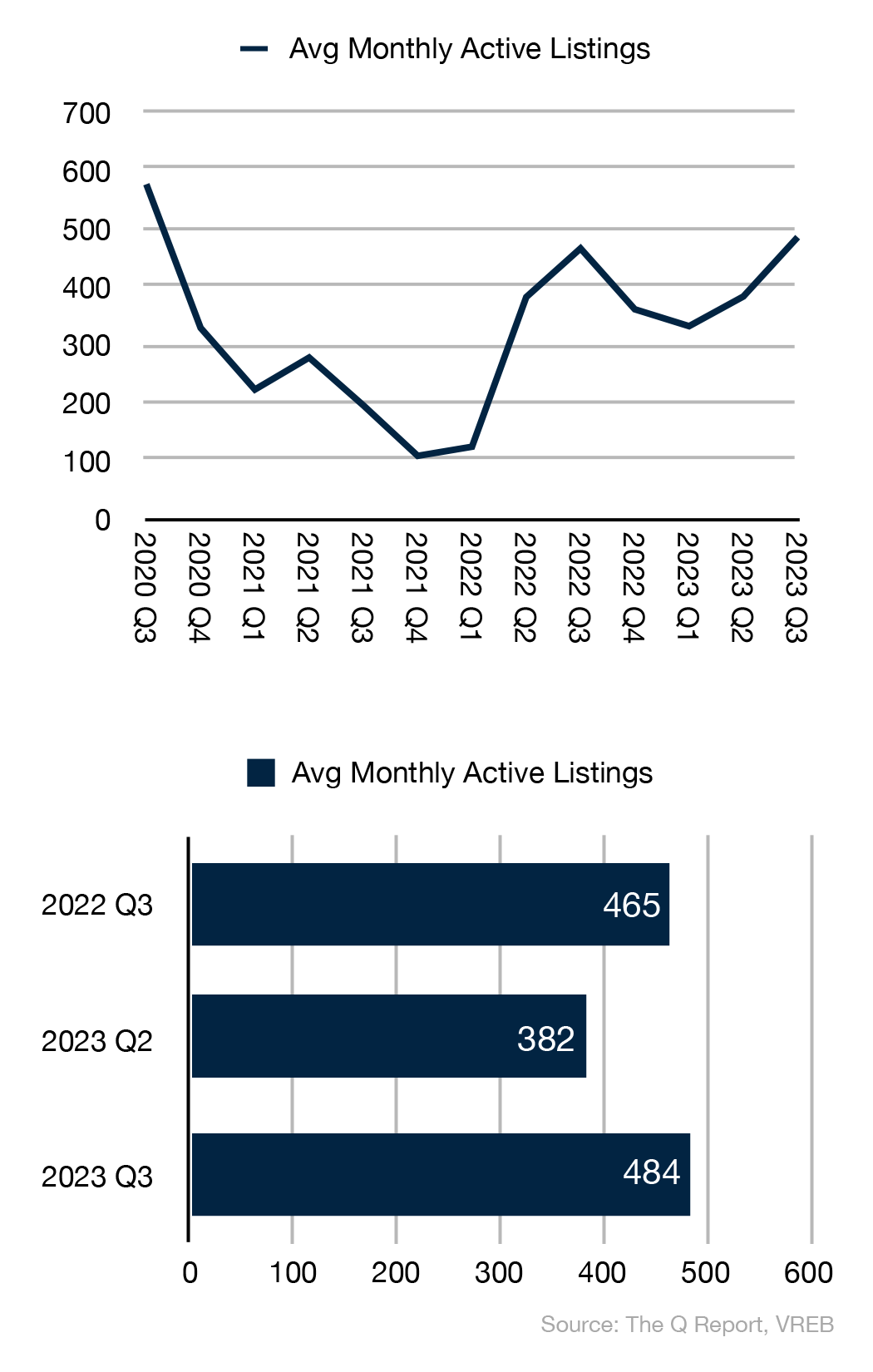

- Q3’s average monthly active listing count is the highest we have recorded for homes priced above $1.5M, more than 2.8 times more than when inventory bottomed out two winters in a row, 2020-21 and again in 2021-22.

- We begin to wonder: at what point do sellers of luxury homes need to start competing with one another on price to attract a limited pool of prospective buyers?

HPI® TRENDS

The MLS® Home Price Index® (MLS® HPI®) is purpose-built to gauge neighbourhoods’ home price levels and trends, using more than a decade of sales data and sophisticated statistical models to define a “typical” home based on the value home buyers assign to various attributes on homes that have been bought and sold. These benchmark homes are tracked across localized neighbourhoods and different types of houses. The Q Report’s HPI® trends compares relative regional price movements around Greater Victoria by tracking the HPI® Composite Benchmark Price across 15 districts, comparing Y/Y price changes.

- Overall, this edition’s HPI Trends shows Y/Y price movements around the region which were modest, with most areas shifting less than 3%.

- Some urban core areas like Victoria and Langford saw HPI index values and benchmark prices drop by a few points

- Highlands and Central Saanich, both composed of a higher proportion of larger suburban/rural/farm properties bucked both trends, recording +9.7% and +7.4% respectively. Why?

- Our HPI analysis uses a ‘composite’ index, which includes single family, condo, and townhouse types. Counteracting movements within different property types for an area can result in unexpected totals.

- For instance, even though detached homes and townhomes were relatively flat in Victoria, the -7% change to the HPI benchmark price for a condo unit netted out to -2.3% overall in the weighted-average composite figure. Compare this to View Royal, where all property types showed a decline, versus Saanich, where all property types showed some degree of increase.

- As we mentioned in our last two editions, the recent data update to the MLS® HPI has resulted in more timely data, though it is still subject to interpretation and analysis. If you’d like to see how this powerful statistical modelling tool can be applied to you unique needs, get in touch to schedule a complimentary consultation.

WHERE’S IT GOING?

- Will we have a spring market in 2024?

- Demand for home ownership among Canadians who still believe in the value of owning real estate continues to fuel the market; ownership is still a widely held goal and cause of FOMO for Millennial buyers.

- BC Premier David Eby’s moves to increase housing supply are steps in the right direction, but current demand won’t wait for those homes to be built, and existing supply will be coveted.

- However, as recession talk ramps up again, and sentiments shared in the media by economists, experts, and talking heads sours, consumer sentiment is likely to follow.

- Conditions in Ontario’s ‘Golden Horseshoe’ continue to deteriorate — will this be a look into the future of western markets?

- The connection between the BoC’s policy rate and housing sales is evidenced in the chart below, provided by the BC Real Estate Association. The BoC has held the door open for itself to further hikes, and at the very least, are signalling ‘higher for longer’ as we look toward 2024.

- As we noted in The Explainer, there are other macroeconomic signals pointing to a Canadian recession. While recession has been signalled by markets for some time, economists only find out about recessions once they are already underway. By way of an example, we have noted yield curve inversions in recent reports, which have strong predictive power for recession, but the length of the lag between the inversion and the recession is an unknown.

- In practical terms, one trend not to be ignored in Q4 is price sensitivity; unless you have something for sale that is really special you can not set an asking price that is beyond what the most recent sales are suggesting — and in shifting markets, we often calculate this period in mere weeks — otherwise, buyers will just say no thanks.

- Lastly, Victoria tends to have lower levels of diversity in our available housing stock. If you miss out on the home on the street or in an area you want, oftentimes you’ll wait a while for a true comparable to appear.

CONCLUSION

Victoria’s real estate market held up well in Q3, but signs of a slowdown are emerging in the data as we head into Q4. Clouds on the horizon suggest a storm could blow this way, but we can’t predict with certainty when or how hard it might come. For the answer to that, we invite you to make sure you’re subscribed to receive the next Q Report — and please share our unique market intelligence with a friend, if you haven’t already.

Of course, the most enduring and unique situation that always requires a deep dive of its own — in a Q Report type of way — is yours. Validate your best options after studying the numbers that affect you, be they short, medium, or long-term.

Market knowledge, experience and skilled professional guidance are your keys for a successful transaction. Produced since 2018, there exists no quarterly analysis of the real estate market like the Q Report. We encourage you and anyone you know to reach out to us any time an authoritative opinion is required.

Do you or someone you know need real estate advice, personalized market insights, a home marketed and sold using the best tools and accurate data? We are available to be your personal resource. Get in touch today.

Subscribe, follow us on your favourite social platform, and reach out any time.

Dirk VanderWal & Fergus Kyne

Newport Realty Ltd.

(250) 385-2033 | info@victoriaqreport.com

Notes

All views and opinions expressed in The Q Report are solely those of its authors, Dirk VanderWal and Fergus Kyne, and do not necessarily represent the views or opinions of Newport Realty Ltd. or the Victoria Real Estate Board. Not intended to solicit parties already under contract. E&OE.

Terms

For a list of terms and definitions used in The Q Report, click here.

Data Analysis

The Q Report’s analysis includes listing and sales data exclusively from the Victoria Real Estate Board’s Multiple Listing Service® (MLS®) ‘Core’, ‘Westshore’, and ‘Peninsula’ regions. Data is analyzed for unconditional pending and completed sales that occurred between 2023/07/01 and 2023/09/30 except where specifically noted otherwise.

Data Sources

BC Real Estate Association

BetterDwelling

BNN Bloomberg

Citified

Daily Hive

Financial Post

Global News

Canadian Real Estate Association

Canadian Mortgage Professional Magazine

CBC News

Richardson Wealth

The Globe and Mail

Times Colonist

Victoria Real Estate Board

Zolo