INTRODUCTION

What Actually Happened.

If you’ve read The Q Report before, you’ve seen us use this phrase, and know it’s not a question. As we reconvene to research and write this edition, as we have been doing for nearly five years, we recognize that we have not witnessed a sea change anything like what we are in the midst of.

Like any asset, real estate is dynamic. We have seen downturns in different areas, but it is rare for people to pop in and out of real estate ownership. When it is time to make a move, what is important is knowing what you ought to pay today, what you can sell for today, and seeing the broader historical context in which those figures lie. That has always been the strength of our analysis.

THE EXPLAINER

Uncertainty vs Certainty and Choosing Your Best Representation

Jumping off from this edition’s introduction, let’s talk about uncertainty. We find ourselves in an adapting market, where our usual ability to make Q Report predictions is in question. However, even in these dynamic times, it’s still entirely possible to move with certainty. A shift in market dynamics such as we are experiencing must be met with a shift in approach for a successful transaction.

As nearly every one of The Q Report’s metrics details a cooling trend, it’s important to keep in mind that this is also a return to balance, from the imbalance that was sparked in the depths of the COVID-19 pandemic. Lack of balance will lead one to fall; a fall doesn’t mean certain death, but likely a bruising. Fortunately, the numbers assure us that those who purchased in the past two years or before are still ahead, even though the trend is turning back down. If you are not selling just after buying, then you bought at a good time. Very few people ‘flip’ homes in our market; it’s risky and stressful.

For those who are seeking certainty — for those serious about buying or selling — deciding upon your representation in this market is crucial. We would like to point out that needing (as opposed to wanting) to buy or sell doesn’t have to equate to desperation. Rather than feeling desperate, you must feel confident that your price is accurate. Your unique situation and your potential offering require unique analysis. Contracting with seasoned professionals who study the data and trends like we do puts you in the best possible position to succeed, and alleviates the sense of uncertainty.

Why should you work with us? First, let’s look at the listing side.

Sellers

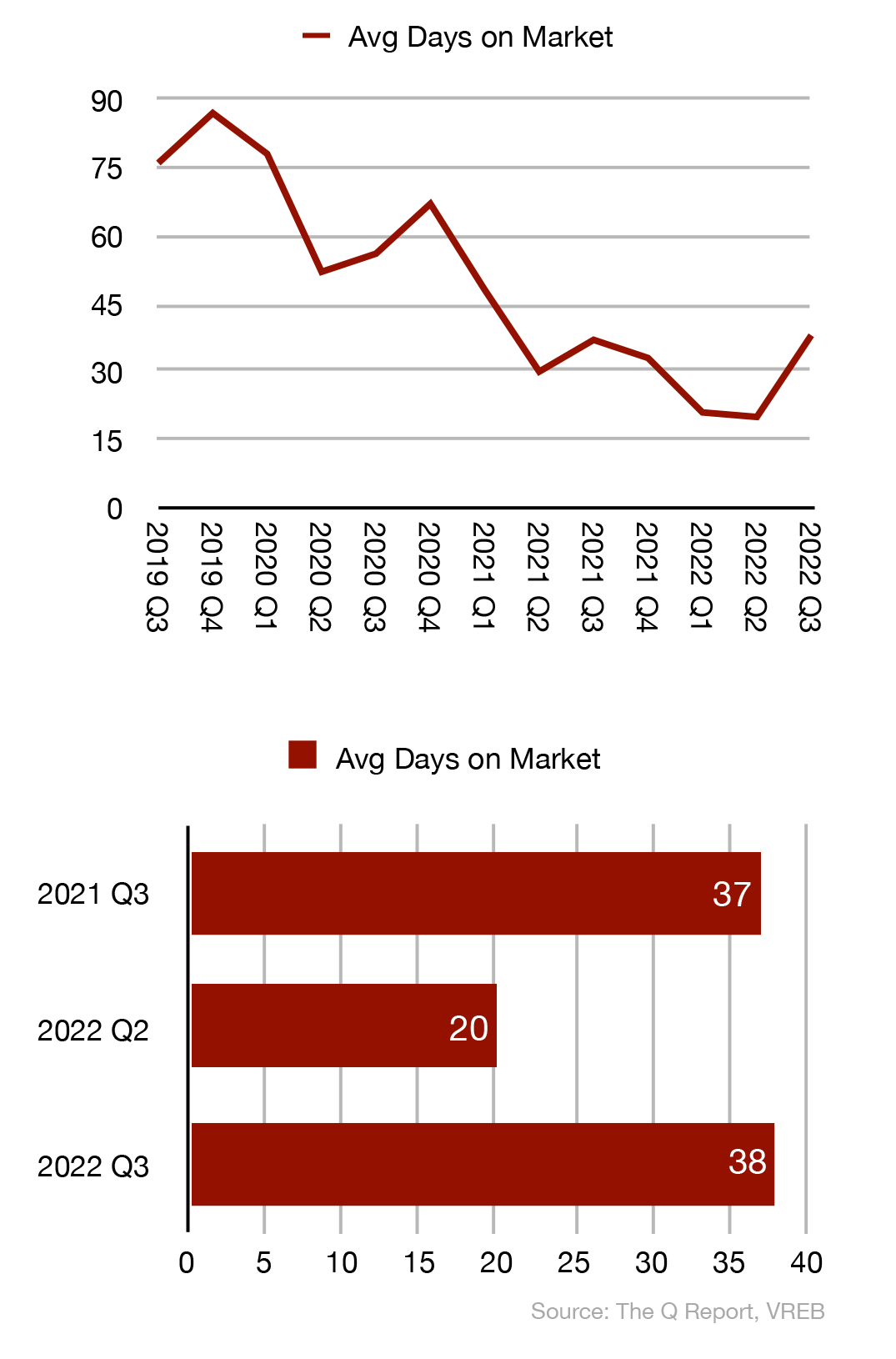

We know empirically that the longer a home sits unsold, the lower the eventual sale price. Applying the concepts from an oft-cited 2016 macrodata study conducted by Zillow, we directly examined all single family home sales from our market area in Q3 and found the local data bore out stunningly, when we analyzed the home sales as two groups, those that occurred in fewer than 21 days, and those that occurred after more than 30 days:

| <21 DOM | >30 DOM | |

| Avg Original List Price | $1,060,275 | $1,144,625 |

| Avg Sale Price | $1,045,450 | $1,035,525 |

| Avg Assessed Value | $956,000 | $930,000 |

| Avg Days on Market (DOM) | 11 | 56 |

| Avg Listing Discount | 1% | 10% |

| Avg Price/SqFt | $557 | $520 |

In our Victoria sampling, the assessed values of both sets of homes were nearly identical, within 2.8%. At sale, both landed close to +10% of assessment. The consistency of these benchmarks suggests that the our analysis represented an ‘apples to apples’ comparison.

However, homes that took longer to sell were listed for an average of 8% more ($1.145M). They spent more than four times longer on market, averaging out at just under two months. After conceding more than $109K, representing a 10% listing discount, they eventually sold for an average of $1.035M.

The other set of properties, priced in tune with the current market, averaged 11 days on market, conceded just 1% of their list price, and achieved 7% higher per-sqft sale price and higher overall sale price at an average of $1.045M. While these sellers concluded their transactions with more cash in their pockets from the sale, this does not even begin to account for the soft costs of their additional mortgage, utility, and property tax payments, not to mention the sellers’ time, anxiety, and energy into cleaning and preparing for eight weeks worth of showings.

We attempted to represent this tale visually, the dark blue block representing the <21 day group of sales, and the light blue block representing the >30 day group of sales:

The price line of the slow sale moves down smoothly over time, from original listing price to ultimate sale price, though a real-world example would most often include a few discrete steps representing price reductions, as sellers attempt to chase the market down, and as the days on market count tallies up, buyers entering the home begin to walk in wondering ‘what’s wrong with it that it hasn’t sold?’

The lesson here is, of course, the critical importance of correct, evidence-based pricing, in a market where sellers are increasingly competing to catch buyers’ attention.

This harkens back to an article we published in our Q3 2019 edition entitled ‘The 5% Difference,’ an explainer on how important it is to nail pricing, with movements of just 5% or less often making the difference between frustration and success. At the time, interest rates were just below current levels, and the market was feeling flat.

Buyers

If you are a serious buyer, you will have two important concerns to consider: not missing out on an ideal home, and not paying too much. We work with homebuyers using a carefully developed and field-tested process that addresses both concerns, including individualized, per-property buyer-side price analysis. Avoid uncertainty and proceed with confidence that comes from being highly informed, educated, and empowered.

MARKET BREAKDOWN

Overview

As sales slowed and listings increased, the market through Q3 was typified by an increasing sense of stalemate: sellers holding out for their pricing, buyers holding back from paying. Supply has increased, though not yet to levels seen during the last major ‘buyers market,’ as some would-be sellers hold off listing in the hopes that a more opportune market will arrive.

Affordability benchmarks show us exactly why there is a gap between buyers and sellers: either prices need to come down, interest rates need to come down, or both, in order to restore objective affordability based on income levels. An $800K mortgage at 2.5% and a $600K mortgage at 5% have nearly identical monthly payments. On its face, this suggests that without downward rate movement, a 25% price correction would be needed to restore equilibrium in this scenario. The looming recession should tame inflation, and drag home prices down further with it, but we won’t be holding our breath for rates to follow the downward trajectory any time in the next year.

In the face of this certain recession, new construction is going to slump. In fact, the slowdown has already begun, with high profile multi-family projects being shelved or delayed in Vancouver and Toronto. Builders for single-family detached homes are going to have a hard time attracting buyers at prices that the builders are essentially stuck with given to baked-in costs, which will put the brakes on that sector as well. Making things worse, several of Canada’s ‘big five’ banks have already stopped lending on development lands.

On the other side of the coin, the country’s lofty immigration targets which intend to bring millions of new Canadians to our shores over the coming decade, in addition to the nearly 700,000 in new population over the past year alone, spell out serious future trouble for housing supply, even though demand is down temporarily as the market adjusts to a new interest rate environment.

No doubt housing policy will dominate the upcoming round of municipal, provincial, and federal elections. And well it should, for there a crisis continues to materialize.

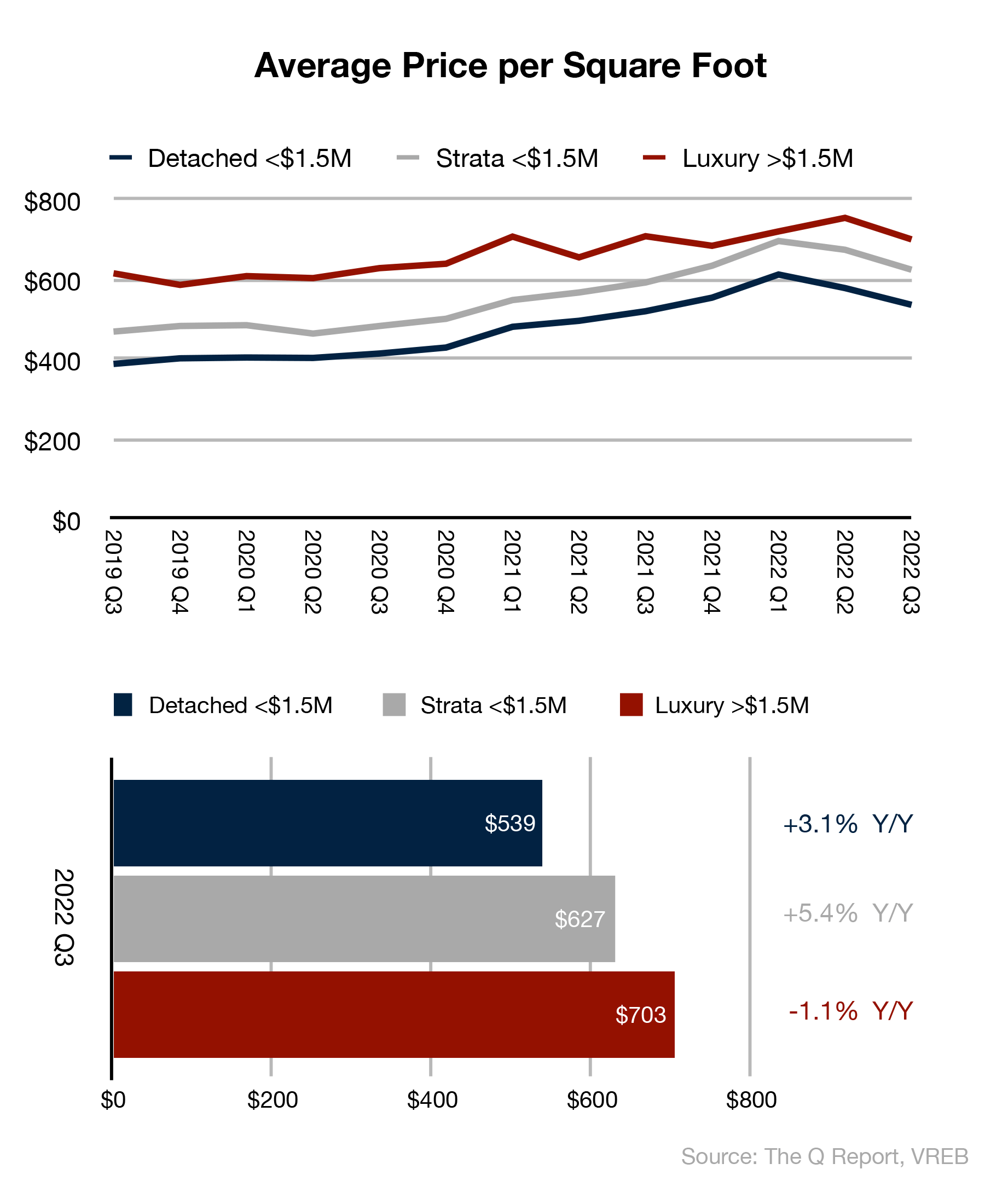

Detached Homes, <$1.5M

The single-family detached home market in Greater Victoria has already seen a 15% drop in median prices from its Q1 peak, though still up slightly Y/Y. Market times are the highest we have seen since 2020, with four times more listing inventory than was available at the end of 2021. The number of sales fell nearly 29% from Q2.

Most notably, we counted a return to a listing discount for the first time in two years — and a big move at that, to 3.6%.

It’s clear from the data that serious sellers are having to market at the right price to attract buyers.

Strata Homes, <$1.5M

Sales of attached homes fared slightly better in Q3, with the median sale price down 10% from the Q1 peak, but still holding up over +11% Y/Y. Average days on market returned to 2021 levels, and listing inventory increased by one third compared to last quarter, ending up around double from its lowest point. As well, with the tightest listing discount at just 2%, strata homes look like the strong suit if you have a hand to play as a seller.

Luxury Homes, >$1.5M

With the cost of borrowing knocking many buyers out of the $1.5M+ space, we saw the number of luxury sales slashed in half in just one quarter. Although we saw a decrease of only 1.1% to median sale prices compared to last quarter for those homes which did sell, listing discounts rocketed to the second-highest level we’ve tracked, suggesting that it required willingness to negotiate in order to secure buyers.

These seemingly contradictory figures are better deciphered by looking at the breakdown of luxury sales by price point:

In Q3, twice as many sales occurred just above $1.5M than the next $250K bracket covering $1.75M-$2M. This is counter to Q1’s trend which actually saw more sales at the higher price point — a full three times more than the Q3 count. Carrying on the trend, earlier in the year we also saw more than twice as many sales in the $2.0M and $2.5M brackets, both of which have dropped to a handful more recently.

Notwithstanding the small but consistent set transacting in the $3M+ range, the dent in purchasing power is definitely pushing activity to the lower end of the higher end.

HPI® TRENDS

The MLS® Home Price Index® (MLS® HPI®) is purpose-built to gauge neighbourhoods’ home price levels and trends, using more than a decade of sales data and sophisticated statistical models to define a “typical” home based on the value home buyers assign to various attributes on homes that have been bought and sold. These benchmark homes are tracked across localized neighbourhoods and different types of houses. The Q Report’s HPI® trends compares relative regional price movements around Greater Victoria by tracking the HPI® Composite Benchmark Price across 15 districts, comparing Y/Y price changes.

Regular readers will have gotten used to seeing Y/Y HPI® index and benchmark value changes in the +20-30% range throughout our recent reports. Although Q3 wrapped up with Y/Y gains in every area once again, the figures were markedly more modest, at mostly 10-15%. But this is year over year — looking at movements within the quarter, the monthly trend has been distinctly downward:

While the index initially treated a change in price direction from rising to falling prices as a ‘blip’ — which we covered in our last report — several months of persistent softening have seen the index now recognize and track as a trend. Below, we’ve charted the composite index change from the end of Q2 to the end of Q3:

As we move through the last quarter of 2022 and into the new year, we expect HPI® Y/Y changes to continue to recalibrate closer to zero. Make sure you’re subscribed to The Q Report for our next update.

CLOSING

Thank you for reading The Q Report. Whether you are a new or long-time reader, we hope our market insights have been valuable, and you would feel comfortable approaching us with your questions or your unique situation.

As the market continues to evolve, if you need to sell, perhaps we could help you appropriately set your expectations using the data analysis employed in the report. Even in markets that favours buyers, buyers are still quick to overlook a property’s shortcomings and present an offer if they feel a sense of value — and the price to get them there may not be as low as you think.

If you need to buy, know exactly what number you should be happy with, and have no regret. We will price on the purchase side with confidence, as though we were pricing a listing for sale.

In either case, our mantra is “there’s nothing wrong with any property that can’t be fixed by the right price.” As conditions evolve by the week and the month, you can count on us to help you find the right price.

Subscribe, follow us on your favourite social platform, and reach out any time.

Dirk VanderWal & Fergus Kyne

Newport Realty | Christie’s International Real Estate

(250) 385-2033 | info@victoriaqreport.com

Notes

All views and opinions expressed in The Q Report are solely those of its authors, Dirk VanderWal and Fergus Kyne, and do not necessarily represent the views or opinions of Newport Realty Ltd. or the Victoria Real Estate Board. Not intended to solicit parties already under contract. E&OE.

Terms

For a list of terms and definitions used in The Q Report, click here.

Data Analysis

The Q Report’s analysis includes listing and sales data exclusively from the Victoria Real Estate Board’s Multiple Listing Service® (MLS®) ‘Core’, ‘Westshore’, and ‘Peninsula’ regions. Data is analyzed for unconditional pending and completed sales that occurred between 2022/07/01 and 2022/09/30 except where specifically noted otherwise.

Data Sources

BC Real Estate Association

Financial Post

Global News

Canadian Real Estate Association

CBC News

The Globe and Mail

Times Colonist

Victoria Real Estate Board

Zillow