INTRODUCTION

Thank you for reading The Q Report for Q2 2023. We said in Q1 that the market should begin to perform in a more robust manner in Q2, based partly on the fact that the Bank of Canada (BoC) seemed to indicate that the flurry of interest rate hikes seemed to have done most of what it was intended to do — slow down inflation. Many of the metrics our returning readers are familiar with indicate that Q2 was typical of a ‘spring market,’ albeit with fewer new listings reported. This lack of inventory is the main reason why we have seen a rise in values in Q2 over Q1, though condos remained relatively flatter.

There’s a lot going on out there, so let’s get into it.

THE EXPLAINER

What ACTUALLY Happened in Q2?

- The big story this quarter was the bounce. A bump in the market. A spring market that met (or exceeded) expectations. We saw a surprising rally, largely driven by consumer confidence on the heels of a period of stabilized interest rates, and low inventory.

- There has also still been a sense of FOMO in the market, especially when prices began to rise against expectations. Even as affordability has gotten even more strained, those wanting to get into the market see rising prices as perhaps their last chance.

- But was it a ‘dead cat bounce’ on the market’s way down? Though it’s too soon to tell, if we take our clues from the financial system right now, the answer looks like conditions there may get challenging before they get better again — which could take a while.

- Macroeconomic figures have continued to surprise to the upside throughout the first half of the year, the BoC’s hand was forced in June, rates went up, and we see more rate hikes on the way. Movements in the bond market are also causing fixed rates to rise.

- OSFI, the banks’ regulator, is trying to clamp down on credit availability, indicating that they believe banks have been too lenient. Don’t be surprised if you see ‘variable rate – fixed payment’ mortgages taken off the menu next year.

- Even without OSFI’s moves to tighten, new credit originations have already slowed to a trickle, down some 80% from early 2022’s highs.

- BoC indicates it has no near term plans to reverse the rate hiking cycle, contrary to consumer expectations that rates would begin to move lower in late 2023. Macklem has indicated that the BoC will not tolerate rising home prices in their battle against inflation, as evidenced by June’s 25 bps hike. A bucket of cold water on Canadians who have enjoyed a decades-long run up on house prices.

- Markets are currently pricing in another hike in July as more likely than not.

- Other signs that affordability is pushing on people: a May survey revealed that nearly half of Canadians reported cutting down on ‘essential’ spending — things like food, clothing, and utilities — in order to keep up with debt payments.

- But don’t be fooled — real GDP (standard of living) isn’t rising.

- Consumer spending is up, yes, but the amount consumers are getting for those dollars isn’t going up in kind.

- Does this sound familiar? Spending more and not getting more? Like maybe the cost of housing?

- Ah, the magic of inflation.

- As the spring market met expectations, so will the summer feel its usual slowdown in the volume of listings and sales. As the pandemic recedes into memory, we find the usual seasonal rhythms of the market returning.

- However, the early days of summer and macro conditions above suggest that this cycle, the slowdown may be a little deeper. We expect a soft, slow summer market in Victoria.

- Back east, honest to goodness bloodletting has begun in the GTA real estate market.

- But will it arrive here? Read on for our look ahead.

MARKET BREAKDOWN

Overview

- As we outlined earlier in the report, the headline story was unexpectedly strong market performance this past spring.

- The bounce felt particularly pronounced against a very soft finish to 2022 and an equally lacklustre start to 2023, with the biggest surprise being a jump in sale prices. Single family homes increased around 10% from their lowest point at the end of 2022.

- Looking at the sales-to-active-listings ratio, we can see consumer demand stoking prices: winter truly saw a brief dip out of ‘sellers market’ territory, but eager buyers were ready to act in Q2, even as we saw standing inventory continue to recover.

- Y/Y comparisons look less exciting, however, with most pricing metrics ending up within a few points of where they were a year ago, at which time the beginning of the rate hiking cycle had already begun to hammer prices.

- Even with recent price increases, detached home prices are still down -9% from the peak, strata -7%, and luxury -4%.

Detached Homes, <$1.5M

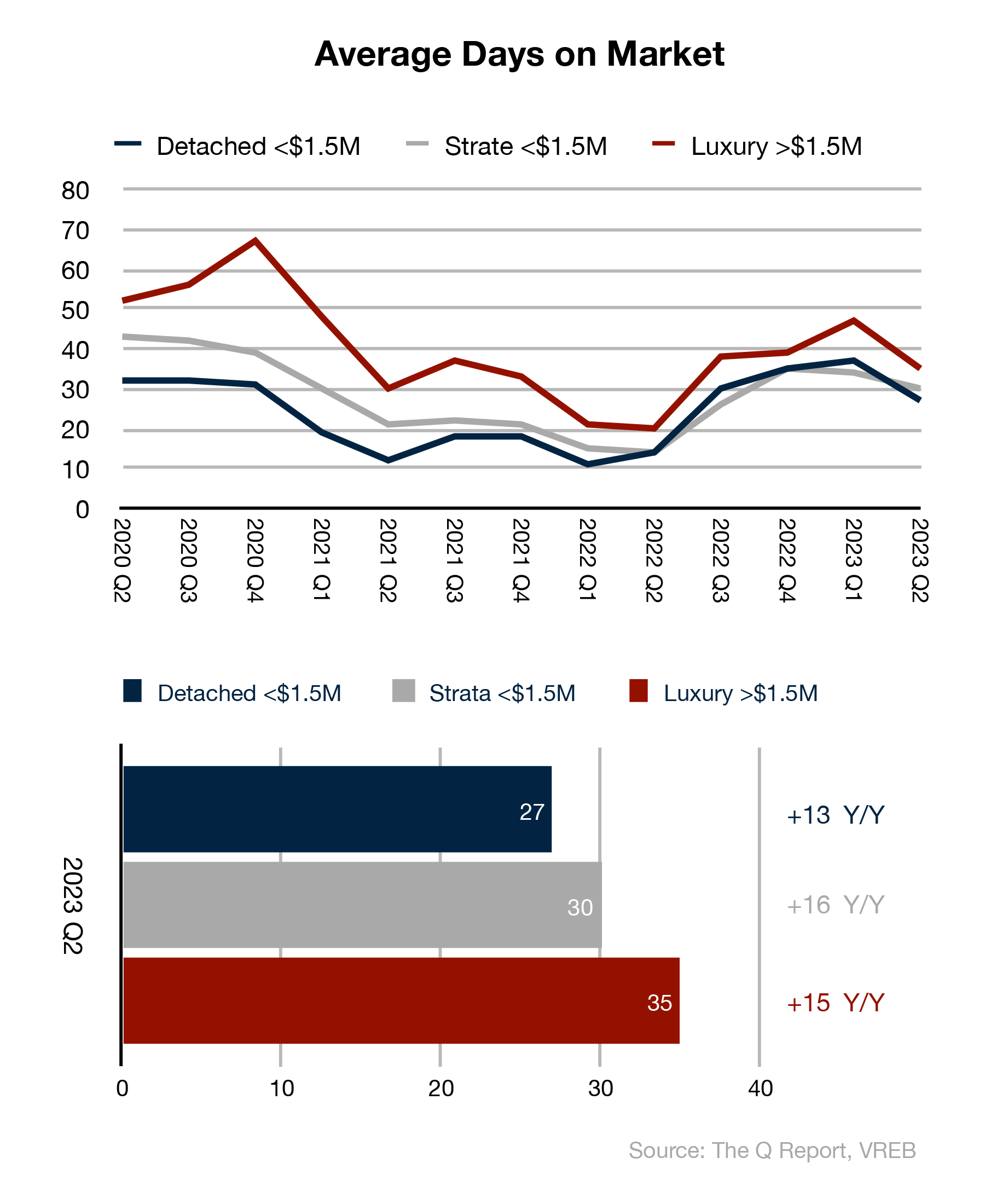

- Every metric we examine shows that Q2 was a classic spring market bump over Q1, but when looked at Y/Y we clearly see that we may be headed for conditions where increased competition among buyers will not be a strong factor. Most notably active listings are increasing. That combined with an increase of nearly two weeks to Days On Market Y/Y during our traditionally hot (spring) market may be a harbinger of cooling conditions for sellers.

Strata Homes, <$1.5M

- A huge bump in sales Q/Q but down slightly Y/Y. With over 50% more active listings Y/Y and fully a fifth more selection Q/Q we can see why anecdotally we are hearing from buyers that the ‘condo’ market feels more accessible. This despite an increase in PPSF and Median Sale Price.

Luxury Homes, >$1.5M

- This is a segment that has experienced less volatility during our time of recording What Actually Happened. However Q2 saw a huge increase in recorded sales — the largest Q/Q jump since the 2020 Covid-related explosion in demand began. Let’s see what happens going forward when money costs considerably more to borrow and high income earners who were feeling very bullish with 2% money are seeing what 6-7% interest rates combined with higher costs for everything, does to their optimism and risk tolerance.

HPI® TRENDS

The MLS® Home Price Index® (MLS® HPI®) is purpose-built to gauge neighbourhoods’ home price levels and trends, using more than a decade of sales data and sophisticated statistical models to define a “typical” home based on the value home buyers assign to various attributes on homes that have been bought and sold. These benchmark homes are tracked across localized neighbourhoods and different types of houses. The Q Report’s HPI® trends compares relative regional price movements around Greater Victoria by tracking the HPI® Composite Benchmark Price across 15 districts, comparing Y/Y price changes.

- The long-awaited June update to the HPI brought back more timely pricing data and other refinements. Our first look at the data reignited our confidence in this immensely valuable statistical tool, as it echoed what our other analysis pointed to.

- Even though every single district is showing a decline of several points Y/Y, the majority are up from January and March’s benchmarks.

- Just what we saw, confirmed again — winter dip, spring rally.

WHERE’S IT GOING?

- Nationally, we expect to see home prices begin to moderate down again in the face of continued interest rate increases.

- Areas in the farther reaches of the Golden Horseshoe are already showing signs of trouble from over-leveraged purchasers getting squeezed.

- But will we feel the same degree of pain in Victoria? Not likely. Or at least not as bad. Why?

- Inventory remains low compared to historical standards.

- Save for 2020, when the world went into lockdown, this year’s Q2 was the lowest quarterly number of new lists in a decade.

- Cyclical mortgage renewals haven’t made as big an impact on the market as expected yet, particularly with a conspicuous absence of ‘distressed’ sellers creating a glut of listings, and it is estimated that around a third of mortgage holders have already been exposed to the impacts of higher rates.

- Of those that do choose to sell when it’s time for them to renew, the majority will be investors, who will suddenly lose their ability for their investment to cashflow in the face of a 40% increase to their primary expense, who are allowed to increase rents by a maximum of 2%. This will create more inventory, particularly condos, but we don’t know how much, or when.

- Most other homeowners are hanging on for now, especially given banks’ apparent reluctance to act on trigger rates.

- We still have not enough homes for people, and people still want to live here. We’ve talked about immigration policy and its relation to the housing crisis, which has made its way into the mainstream discourse. However, new Canadians are more likely to be renters than purchasers, and many newcomers tend to end up in larger centres like Vancouver, Toronto, Calgary – so the present influence on our market is secondary in nature: rental market inputs, and purchasers coming to Victoria from those three ‘feeder’ markets.

- Housing starts continue to decline, as permitting remains difficult, costs are up immensely, and the construction sector deals with a widespread labour shortage.

- Inventory remains low compared to historical standards.

- Perhaps the best case scenario is an extended period of stagnation in home prices, like in the ‘90s and early ‘00s, where the rest of market fundamentals can ‘catch up’ to home prices.

- With rapidly rising/falling prices taken out of the equation, real estate becomes more about moving when life dictates, and not trying to time the market.

- This isn’t a bad thing, and may help treat our national fetishism with the real estate market. If you want to day trade, go to the stock market. Not the real estate market.

- Even as demand softens and prices flatten, we will continue to see well priced and well presented homes sell successfully. The real key is in defining what ‘well priced’ means for a given market. If it’s important for you to know the right price to buy or sell given all that’s shifting in the housing market right now, we are your best call.

Do you or someone you know need real estate advice, personalized market insights, a home marketed and sold using the best tools and accurate data? We are available to be your personal resource. Get in touch today.

Subscribe, follow us on your favourite social platform, and reach out any time.

Dirk VanderWal & Fergus Kyne

Newport Realty | Christie’s International Real Estate

(250) 385-2033 | info@victoriaqreport.com

Notes

All views and opinions expressed in The Q Report are solely those of its authors, Dirk VanderWal and Fergus Kyne, and do not necessarily represent the views or opinions of Newport Realty Ltd. or the Victoria Real Estate Board. Not intended to solicit parties already under contract. E&OE.

Terms

For a list of terms and definitions used in The Q Report, click here.

Data Analysis

The Q Report’s analysis includes listing and sales data exclusively from the Victoria Real Estate Board’s Multiple Listing Service® (MLS®) ‘Core’, ‘Westshore’, and ‘Peninsula’ regions. Data is analyzed for unconditional pending and completed sales that occurred between 2023/04/01 and 2023/06/30 except where specifically noted otherwise.

Data Sources

BC Real Estate Association

Financial Post

Global News

Canadian Real Estate Association

CBC News

CTV News

Richardson Wealth

The Saretsky Report

Storeys

The Globe and Mail

Times Colonist

Vancouver Sun

Victoria Real Estate Board