INTRODUCTION

Thank you for reading The Q Report. This edition breaks down what actually happened in the headline-grabbing real estate market in early 2022 with a full analysis of the quarterly market numbers, and a backgrounder on the national and international macro forces that are influencing homebuyers’ decision making at the local level.

After last quarter’s deep dive on inventory levels, we made the decision to add average monthly active listings per quarter to our metrics going forward, which will add one more dimension of data to help illuminate the stories behind the numbers.

While we did successfully predict the white-hot market conditions for property sellers in January and February, March may have signalled the beginning of a levelling off of demand. Q2 may well mark a turning point from the zenith of increasing property values. Read on to find out more.

OPPORTUNITIES: Q1 2022

Anticipating the shift in conditions looking into Q2, here are the areas of opportunity we see for players in the near-term market:

Buyers:

Cash is king: Those with equity, less affected by rapidly declining borrowing power, will be better positioned to take on the Q2 market. If you’ve already sold, you may be facing less competition to buy back in.

Rate holders: Conversely, buyers who have a 90 or 120-day rate hold currently in place are well advised to act quickly if stress-testing above 6% will put them out of the game.

Either way, if you need a plan of attack to secure a purchase this quarter, drop us a line to get started.

Sellers:

Spring Sale: There is still a window of time to approach the market before the full effect of rate hikes take effect, as there is typically a 3-4 month lag while buyers are able to take advantage of existing rate holds. This is also the time of year when listings see the highest number of buyers active in the marketplace. If you’d like your listing to receive maximum exposure and precise pricing based on thoroughly analyzed data, give us a call today.

Rental Restricted Stratas: The exemption under BC’s Speculation and Vacancy Tax that applied to rental-restricted strata properties expires as of 2022. If you’d like to avoid the sting of having your equity taxed away, why not reach out to us for a consultation and market evaluation.

Investors:

Feeling on Hedge: Investors know that real estate provides an excellent hedge against inflation; those with liquidity can act to protect their financial assets though this inflationary cycle, and, although rents have not risen in lockstep with sale prices, landlords offering units in the current rental market will find great returns available.

THE EXPLAINER

With inflation and rising interest rates making daily news as we close out Q1 of 2022, we have been fielding questions on where they are, and where they’re going. Naturally, we thought it would make a great topic for this edition of The Explainer.

How is Inflation Measured?

Inflation is primarily measured by tracking the consumer price index (CPI). This is analogous to the home price index (HPI®), which will be a familiar concept to returning Q Report readers. And, similar to the way that the HPI® tracks the characteristics and values of a number of ‘notional’ homes over time, the CPI tracks the value of a notional ‘basket’ of consumer goods and services over time.

Here’s the breakdown of the CPI’s current take on Canadian consumer spending:

As it relates to real estate specifically, you can see that the largest item in the basket is shelter. Note that this does not account for actual purchase prices of homes, but rather the cost to carry them, either through rent or mortgage costs.

Like most of The Q Report’s metrics, the CPI compares Y/Y changes to the total value of the basket. If this January’s basket cost 5.1% more to procure than the same set of goods and services last January (and it did), then it is said that CPI inflation is at 5.1%.

If it seems like a large increase to be paying 5% more on your total cost of living compared to a year ago, you’re thinking what most of us are already feeling. To put it another way, every dollar you put in the bank a year ago will only buy 95 cents worth of stuff today. Clearly, high inflation is a problem, but the Bank of Canada (BoC) knows that a certain amount of inflation is healthy, as long as it allows the economy to grow at a reasonable rate without everyone feeling like their money is shrinking.

Inflation vs Rates

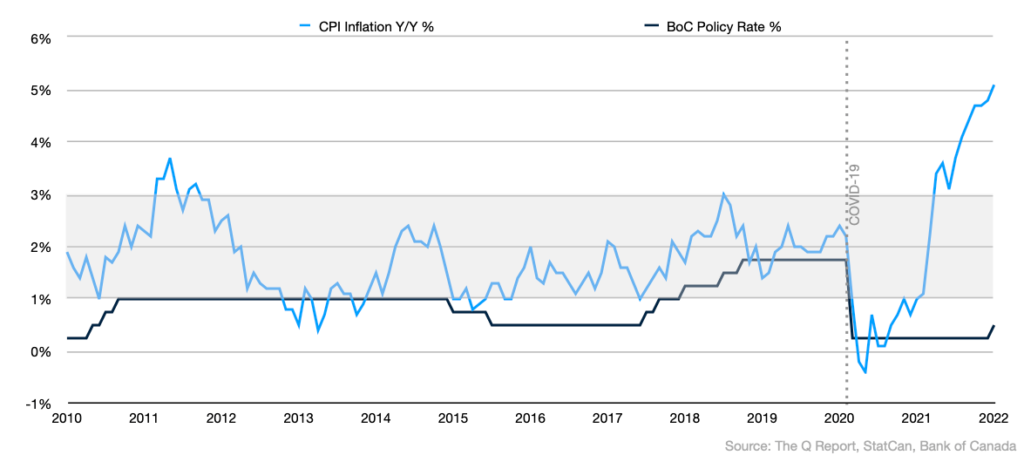

So, since the early ‘90s, the Bank of Canada has adopted inflation targeting, aiming to keep inflation as close as possible to the 2% mid-point of a target range of 1%-3%. This policy has been wildly successful, particularly over the past decade pre-pandemic, and has earned the BoC a great deal of credibility. This graph shows the rate of inflation from 2010 onwards, with the grey area representing the target range.

Let’s say we add the BoC’s policy interest rate to the same graph, below. In tandem with other stimulus measures, the BoC committed to keeping its policy rate pinned down near zero to ensure the economy would weather the pandemic and recover. And recover it has. Coming through 2021, we see the ‘uh-oh’ moment building as inflation ramps up.

There is no shortage of talk about the cause of this inflation; most economists agree the bulk of it is credited to an unfortunate overlap of supply chain constraints and increased demand, as the world’s economy attempts to gear back up after a period of forced convalescence, while at the same time consumers want to quickly return to their pre-pandemic lifestyle, all against the backdrop of an unexpected war and its spillover effects on commodity prices and consumer confidence.

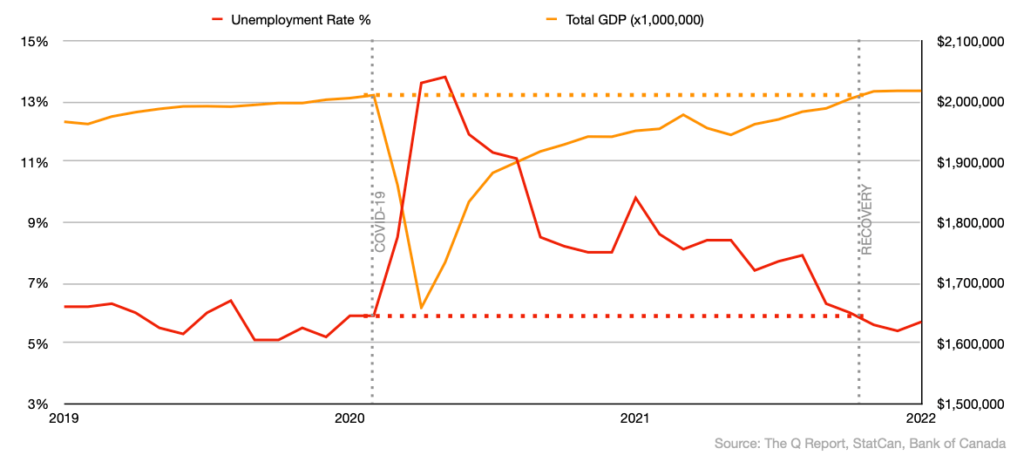

Studying the numbers, what’s interesting to realize is that regardless of where mask mandates, vaccine cards, transmission rates, or hospitalizations are at, as far as the Canadian economy is concerned, COVID is over. With the benefit of 20/20 hindsight, we can see that GDP and unemployment both returned to their pre-pandemic levels at approximately the same time in 2021Q4:

No surprise, then, that the past six months in the real estate market have been like no other. Economic capacity was back, while interest rates remained at 1/7th of where they had been holding for over a year before the pandemic.

Ever since inflation broke out of the target zone before the end of last year, the Governor of the BoC has made it clear that the low rate policy has more than served its purpose, and we can all expect to see rates climb in the near term.

But How Much?

How much rates can or will increase is being hotly debated. We have expressed the opinion here in The Q Report that the rise is more likely to be steady than steep. One of the primary reasons for this stance is Canadian households, and the government itself, are heavily leveraged. With Canadian debt to GDP presently running at well over 100%, that debt burden could multiply the effect of rapid rate hikes more quickly and powerfully than the last inflationary cycle in the early 90s, when the debt to GDP ratio was closer to 70%. During the early ‘80s hyperinflation and double-digit interest rate crisis, debt to GDP was just 40%. In the current environment, the policy rate likely won’t need to exceed 2% to rein in the current cycle of inflation, however, this would still mean around six quarter-point hikes.

As of this writing, bond markets have been ascending rapidly, and fixed mortgage rates have already doubled from last year’s historic lows. This points to a peculiarity of rising rates: they can directly backfire on inflation. Because shelter costs make up the largest portion of the CPI, an increase in mortgage carrying costs naturally pushes CPI inflation up.

Housing Outlook

With rate movements already underway adding hundreds of dollars to mortgage payments for purchases at prices already 20%+ higher than they were a year ago, combined with the inflationary price pressure consumers are already facing at the pump and at the store and shrinking savings, we expect demand to soften noticeably, especially from investors (who we highlighted in our last report), and buyers who are heavily leveraged.

While some economists are calling for price corrections on order of 10%, 20%, or even 40%, most are considering the national market. Victoria remains one of (if not the) most under-inventoried housing markets in the country; even with a 20-30% reduction in buyer demand, it will still take a long time for the number of sellers to outnumber buyers, which is when they have to compete by lowering their prices. However, this will be balanced by the increased cost of borrowing, which will hold down consumers’ widespread willingness to pay record high prices in the second half of 2022.

There are many unknowns at this point. One thing is for sure: we are heading into uncharted territory, and it promises to be another — pardon the phrase — unprecedented year. Keep reading The Q Report for analysis you won’t get anywhere else.

MARKET BREAKDOWN

Overview

Our look back at this quarter’s numbers show the continued results of extraordinarily low listing supply: market times down by half across all segments, a reduction in the number of sales solely due to inventory constraints, and upward pressure on pricing due to supply/demand mismatch.

The spread in price per square foot (PPSF) between property types tightened yet again, with strata properties nearly reaching the same average PPSF as our luxury segment — buyers just get fewer of those square feet, unfortunately. We also saw listing discounts plunge deeper into negative territory as average sale-to-list price ratios reflected a large number of multiple offer sales driving prices up due to buyer competition for everything below $1.5M.

Housing starts were up again in Q1, but with buildable land being scarce in the CRD, the lion’s share is once again in multi-family development.

Detached Homes, <$1.5M

We witnessed the perfect storm of conditions we predicted — high demand fuelled by cheap credit, matched with a scarcity of available homes — which led to these extraordinary outcomes.

- The average sale-to-list price ratio was +8.5% (meaning listing discount of -8.5%).

- Quick sales were the expected norm, with the lowest days on market count we have ever recorded, propped up only by the ubiquity of delayed offers.

- Record high sale prices, with median and PPSF both up by 26% Y/Y.

Strata Homes, <$1.5M

Attached homes continued to perform very well this quarter as first-timers FOMO’d their way into the market, creating competition, evidenced by the lowest listing discount we’ve ever seen for strata, lowest market times, and the highest ever median sale price, once again leading the pack in Y/Y growth.

But with that median price now in the mid-$600s and PPSF edging to $700 for the first time ever, as mortgage rates hit 4%, the monthly carrying cost of that ‘average’ two-bedroom condo will add up to an eye-watering $3,600. We expect that for aspiring first-time homeowners, this will take a bite out of demand.

Luxury Homes, >$1.5M

The luxury segment saw a distinct return to nearly identical conditions that were in place this time last year. Over the course of 2021, luxury sales slowed slightly, allowing inventory to rebuild in this segment, and causing temporary softening in median prices, PPSF, market times, and listing discounts. However, the apparent return of higher demand in 2022Q1 reversed these trends and put us back into zero listing discount territory, bringing along shorter market times and slightly higher median sale prices for homes over $1.5M. Overall, however, median sale price for this segment has not seen the kind of increases that have occurred at lower price points.

HPI® TRENDS

The MLS® Home Price Index® (MLS® HPI®) is purpose-built to gauge neighbourhoods’ home price levels and trends, using more than a decade of sales data and sophisticated statistical models to define a “typical” home based on the value home buyers assign to various attributes on homes that have been bought and sold. These benchmark homes are tracked across localized neighbourhoods and different types of houses. The Q Report’s HPI® trends compares relative regional price movements around Greater Victoria by tracking the HPI® Composite Benchmark Price across 15 districts, comparing Y/Y price changes.

This quarter, the HPI® price trend we have been documenting for over a year stuck around: the region’s least urban areas continued to lead Y/Y index price growth, in a big way.

Numerous employers are bringing staff back into offices after B.C.’s decision to lift mask requirements and capacity limits, and, although many workers are attempting to negotiate ongoing remote work arrangements, for others, 2022 means the return of the commute, which will tarnish the lustre of ‘the quiet life’ outside of the city. This shift is happening in tandem with the erosion of affordability in those areas; Metchosin, Highlands, and North Saanich already have composite benchmark prices well above the regional average, pushed further by higher financing costs.

We will be interested to see if they will continue to see the demand and resulting price pressure, and if so, for how long. Overall, even if HPI® index value growth flattens out, Y/Y comparisons will still take at least another quarter to return to the range of annualized gains we were used to seeing before 2021. We hope you’re subscribed to receive our next edition to see what happens.

If you’re curious how the powerful, granular, neighbourhood-level data in the full MLS® HPI® dataset can be put to work for you to inform your specific pricing decision or situation, drop us a line.

LOOKING AHEAD

The Q Report has always proudly shown what actually happened behind each quarter’s numbers, and we have always used our analysis to move our readers and clients forward in the right direction. However, it is a particularly difficult time to predict with confidence where the local real estate market is headed, as many overlapping factors which we explored in depth in this edition are having unpredictable effects on the sale of increasingly commodified homes.

Market forecasts from January to March have shifted palpably. While we are unlikely to see a cratering of our market, as ‘except in Victoria’ is a caveat we are used to hearing when it comes to predictions about the Canadian real estate market and whatever ‘bubble’ may exist. Knowing that Vancouver Island and Victoria continue to be among the most desirable and sought after destinations for relocating Canadians, whatever softening we see in 2022 will not be as dramatic as in other markets. However, the cost of borrowing will push demand down in the latter half of the year if current trends continue. We will see fewer offers on listings, and expect the number of ‘inexplicable’ sale prices to drop off significantly. We expect a decrease in delayed offers as a listing strategy. The return of actual listing discounts will not be far behind, but the timeline will be dependent upon how aggressively the BoC moves the prime rate to combat inflation over the course of Q2-Q3, and how the bond market responds to ongoing global concerns.

For now, it remains a seller’s market in Victoria, defined by the continued lack of listing inventory which is a primary factor in keeping values high, with a good number of qualified buyers still in the market competing for not enough listings. Investors who made up a larger than usual percentage of buyers in 2021 will account for fewer sales in 2022, as will first-time buyers of single family homes. The baseline qualification, stress test, and cost of borrowing will prove to be too much for these segments in the face of further increases in rates.

At press time, we still do not have any specific details of BC’s recently announced ‘Homebuyer Protection Period,’ but it will likely come too late to ‘help’ a market that is showing signs of slowing down. BC’s provincial Real Estate Association called for a mandatory five-day period before offers to allow buyers time to conduct the due diligence that the Housing Minister seems to think is lacking. Allowing a rescission period for buyers will certainly introduce new uncertainties into our market, and unintended consequences, but without massive increases to listing inventory, we see any moderating effect on the market as unlikely before the law of supply and demand kicks right back in.

How we can help

We appreciate you taking the time to read The Q Report. Being informed on the value of your largest financial asset — and especially being informed before stepping into any transaction — with solid, verifiable data, have taken on greater importance than ever.

As not only market experts and ‘numbers guys,’ but also award-winning, experienced, skilled and trained veteran real estate agents at one of Victoria’s top boutique firms, we are your best bet for maximizing the opportunity in your next move. Contact us now to chat about your needs, and find out how we can apply our data-driven approach to your unique situation.

Dirk VanderWal & Fergus Kyne

Newport Realty | Christie’s International Real Estate

(250) 385-2033 | info@victoriaqreport.com

Notes

All views and opinions expressed in The Q Report are solely those of its authors, Dirk VanderWal and Fergus Kyne, and do not necessarily represent the views or opinions of Newport Realty Ltd. or the Victoria Real Estate Board. Not intended to solicit parties already under contract. E&OE.

Terms

For a list of terms and definitions used in The Q Report, click here.

Data Analysis

The Q Report’s analysis includes listing and sales data exclusively from the Victoria Real Estate Board’s Multiple Listing Service® (MLS®) ‘Core’, ‘Westshore’, and ‘Peninsula’ regions. Data is analyzed for unconditional pending and completed sales that occurred between 2022/01/01 and 2022/03/31 except where specifically noted otherwise.

Data Sources

Altus Analytics

Bank of Canada

BC Real Estate Association

Bloomberg

Financial Post

Canada Mortgage and Housing Corporation

Canadian Real Estate Association

CBC

International Monetary Fund

The Globe and Mail

Oxford Economics

Statistics Canada

Victoria Real Estate Board

Hi Dirk and Fergus…I happened to come across this article and after reading it, wanted to commend you both on an excellent job you’ve done in your analytics and presentation. This kind of professionalism is on an intellectual level that I support and yet find so lacking in our industry today. I hope you don’t mind including me on your mailing list for future Q Reports. After 45 years in real estate, I am still an open mind to learning.

Continued success and thank you for your efforts,